The Core Question

Most ML applied to finance asks: "Can we predict tomorrow's return?" This project asks a harder question: "Does short-term momentum cause tomorrow's return, or does it just correlate with it?"

The distinction matters enormously. A spurious correlation disappears when market conditions change. A causal relationship: if it exists: is structural and should be more robust. We use Double Machine Learning (DML), a method from econometrics, to answer this causally.

Method: Double Machine Learning

DML (Chernozhukov et al., 2018) estimates causal effects in the presence of high-dimensional confounders using a two-stage approach:

- Residualize the treatment: Fit a ML model to predict the treatment (3-day momentum) from all confounders. Compute residuals.

- Residualize the outcome: Fit a ML model to predict the outcome (next-day return) from all confounders. Compute residuals.

- Causal estimate: Regress outcome residuals on treatment residuals. The coefficient is the Average Treatment Effect (ATE): the causal effect of momentum on return.

Cross-fitting with K-folds prevents overfitting from biasing the causal estimate. Conditional ATE (CATE) is also estimated per stock to capture heterogeneous effects.

Features Used

- Return: daily percentage return

- Momentum_3: 3-day return difference (treatment variable)

- Volatility_3: 3-day rolling standard deviation (confounder)

- MA_3, MA_5: 3-day and 5-day moving averages (confounders)

- VolumeLog: log-transformed volume (confounder)

- NextReturn: next-day return (outcome variable)

Data pulled from yfinance for 5 tickers: AAPL, MSFT, JPM, AMZN, XOM (2019–present).

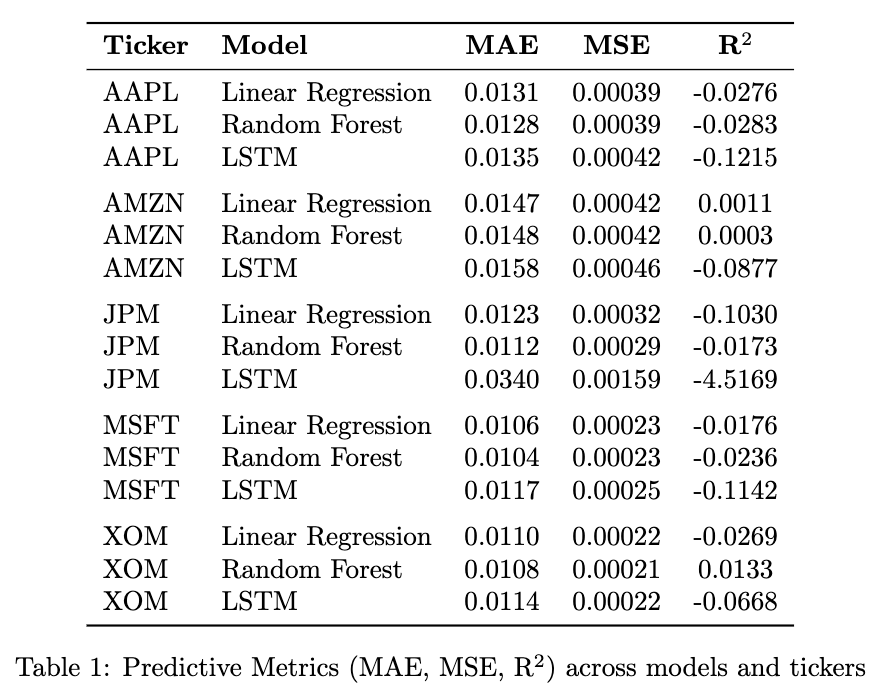

Predictive Benchmarks

In parallel, we benchmark traditional predictive models to understand how much of the return variance they capture: and compare to the DML causal estimate:

| Model | Approach | Metric |

|---|---|---|

| Linear Regression (OLS) | Predictive | MAE, MSE, R² |

| Random Forest | Predictive | MAE, MSE, R² |

| LSTM (2-layer, early stopping) | Predictive | MAE, MSE, R² |

| LSTM Ablation (base/deep/wide/deep-wide) | Architecture study | Training/val loss curves |

| DML (our method) | Causal | ATE, CATE per ticker |

References

- Chernozhukov et al. (2018). Double Machine Learning for Treatment and Structural Parameters. The Econometrics Journal.

- Gu, Kelly & Xiu (2020). Empirical Asset Pricing via Machine Learning. Review of Financial Studies.

- Athey & Imbens (2015). Causal Inference for Statistics, Social and Biomedical Sciences.